What Is an ICHRA? The Government Contractor's Plain-English Guide

When was the last time your employees actually chose their own health insurance?

If you're running a government contract, chances are the answer is "never." You pick a group plan, you negotiate rates at renewal, and your employees take what they get. Even if the network doesn't cover their doctor, the deductible doesn't fit their budget, or the premium eats a bigger slice of their paycheck every year.

There's a better model. It's called an Individual Coverage Health Reimbursement Arrangement, or ICHRA, and it's quietly reshaping how employers across the country fund health benefits. For government contractors subject to the Service Contract Act (SCA), ICHRA isn't just a trend worth watching. It's a compliance-friendly tool that can turn a complex fringe benefit obligation into a genuine advantage.

Here's what you actually need to know.

What Is an ICHRA?

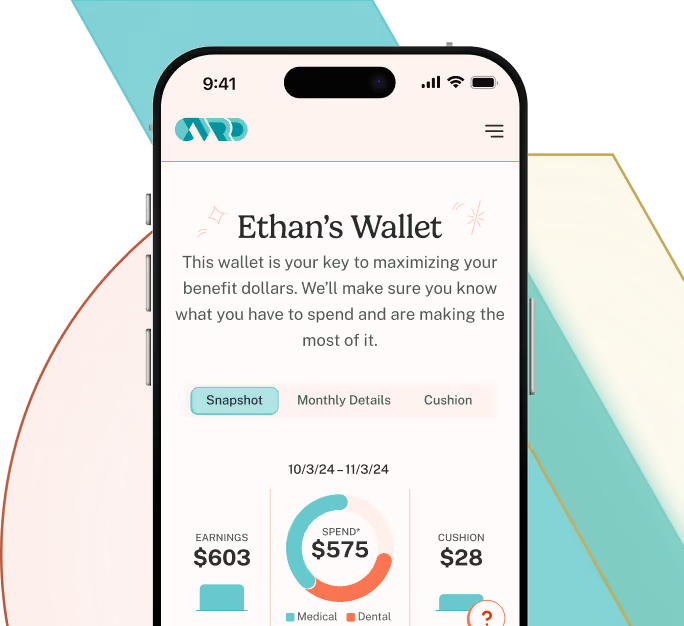

An ICHRA (pronounced "ick-rah") is an employer-funded account that reimburses employees for individual health insurance premiums and eligible medical expenses on a tax-free basis.

Instead of the employer buying one group health plan for the entire workforce, the employer sets a monthly allowance, and each employee shops for their own coverage on the individual market. They pick the plan, the network, and the premium level that fits their life. The employer reimburses them up to the allowance. No one is stuck in a plan designed for the median employee.

ICHRA was established by federal regulation in 2019 under the Trump administration's Executive Order 13813 and took effect for plan years beginning January 1, 2020. It replaced and expanded earlier restrictions on Health Reimbursement Arrangements, allowing employers of any size to offer them without contribution limits.

The mechanics are simple:

- Employer sets an allowance. Any dollar amount within ACA compliance, differentiated by employee class if desired.

- Employee selects an individual plan. On the public exchange, private market, or off-exchange.

- Employee submits documentation. Proof of enrollment and expenses.

- Employer reimburses. Up to the allowance, tax-free for both parties.

Think of it as the 401(k) of health benefits. Instead of the employer choosing one pension plan for everyone, the employee directs the dollars toward the coverage that works for them.

Why Does This Matter for Government Contractors Specifically?

Most ICHRA guides are written for general employers. They don't mention the Service Contract Act. They don't explain Health & Welfare fringe dollars. And they definitely don't explain what happens when your bid price is built around a specific H&W rate and your group plan renewal comes in 15% higher than last year.

Government contractors face a different set of pressures.

Under the McNamara-O'Hara Service Contract Act of 1965 (SCA), contractors performing federal service contracts over $2,500 are required to pay workers prevailing wages and provide fringe benefits, or an equivalent cash payment, as specified in the DOL wage determination attached to the contract. The fringe benefit component is typically expressed as a dollar-per-hour rate for Health & Welfare (H&W) benefits. See 29 CFR §§ 4.6 and 4.170.

Here's the problem with traditional group insurance in this context: the group plan has a fixed cost structure, but your H&W fringe obligation is a per-employee-per-hour amount. When those numbers don't match, and they often don't, you eat the difference, pay it out in cash, or scramble to restructure benefits at renewal.

Group plans also don't give you flexibility across employee classes. A large SCA contractor might have IT professionals in Virginia, maintenance technicians in Texas, and security personnel in California. Each with different wage determinations, different benefit expectations, and different market rates for individual coverage. One group plan serves none of them particularly well.

ICHRA changes that equation fundamentally.

Does ICHRA Qualify as a Bona Fide Fringe Benefit Under SCA?

Yes. When properly structured, ICHRA qualifies as a bona fide fringe benefit under the SCA.

This is the question most GovCon HR teams ask first, and it's the right one to ask. The DOL has established specific criteria for what counts as a "bona fide" fringe benefit under 29 CFR § 4.171. A benefit plan must:

- Be specified in writing and communicated to employees in writing

- Have a primary purpose of providing benefits to workers

- Constitute a legally enforceable obligation

- Require irrevocable contributions to a trustee or third party (no less than quarterly)

- Include a definite formula for determining contributions and benefits

An ICHRA, administered through a qualified third-party administrator, meets all of these criteria. The employer's contributions are made through a structured plan document, administered independently, and communicated to employees in writing. Employer contributions made to the ICHRA plan count toward the contractor's H&W fringe benefit obligation under the SCA wage determination.

However, meeting the general ICHRA rules is only part of the equation for government contractors. SCA compliance introduces additional requirements around how fringe contributions are calculated, allocated, and documented that go beyond what standard ICHRA administrators are built to handle. These include per-employee fringe tracking against specific wage determinations, real-time reconciliation of H&W spend across multiple contracts, and audit-ready reporting that satisfies DOL scrutiny. Most ICHRA platforms were designed for commercial employers and simply don't account for these layers of complexity.

One important nuance: if an employee declines the ICHRA (i.e., opts not to enroll in individual coverage), the contractor still has an obligation to provide the fringe benefit. That means either through alternative bona fide benefits or as a cash equivalent payment. The DOL has been explicit on this point: merely offering a benefit without the employee receiving it does not satisfy the fringe obligation. See DOL All Agency Memorandum No. 220 (March 2016).

How Is ICHRA Different from a Group Health Plan?

The clearest way to explain it: a group plan is a defined benefit. An ICHRA is a defined contribution.

With a group plan, the employer bears the risk. You commit to a plan design, negotiate rates annually, and absorb increases. Your employees get limited choices, typically two or three plan tiers, all tied to one carrier and one network. When the group's claims experience runs hot, renewal rates climb. When an employee's doctor isn't in-network, they're out of luck.

With an ICHRA, the employer defines the budget. That's where the financial exposure ends. The employee takes that allowance into the individual market, which is the largest health insurance risk pool in the country. Individual market premiums trend at a meaningfully lower rate than group market premiums. Urban Institute data suggests the average annual growth trend for individual plans was under 2% between 2019 and 2025, versus more than 5% annually for group coverage over the same period.

What Are the ICHRA Employee Classes for GovCon Employers?

One of ICHRA's most valuable features for government contractors is the ability to segment employees into different classes and offer different allowance amounts to each class.

The federal rules permit 11 employee classes, including:

- Full-time employees

- Part-time employees

- Seasonal employees

- Employees covered by a collective bargaining agreement

- Employees in different geographic locations

- Salaried vs. hourly employees

- Employees working outside the U.S.

- New employees in a waiting period

For a contractor with operations across multiple states, or with both SCA-covered workers and exempt professional staff on the same contract, this is significant. You can set different ICHRA allowances for your SCA-covered hourly workforce and your exempt administrative employees. You can align allowances with the specific H&W fringe rates based on contract and geographic location. This is the kind of flexibility a one-size-fits-all group plan can never offer.

Note: Employers cannot offer an employee both an ICHRA and a traditional group health plan. Each class receives one option or the other.

Is ICHRA ACA Compliant?

Yes. ICHRA is designed to work within the ACA framework, not around it.

For employers with 50 or more full-time equivalent employees, called Applicable Large Employers (ALEs), offering an ICHRA counts as an offer of minimum essential coverage under the ACA's employer mandate (§ 4980H). If designed to meet affordability standards, it also counts as offering minimum value, satisfying both prongs of the employer-shared responsibility requirements.

For 2026, the ACA affordability threshold is 9.96% of household income. An ICHRA is considered affordable if the employee's net cost for the lowest-cost silver plan in their area doesn't exceed that percentage of their household income. Employers can use DOL-approved safe harbors, including rate of pay, prior-year plan data, and location-based benchmarks, to determine affordability.

One critical point: employees who receive an affordable ICHRA offer will no longer be eligible for ACA premium tax credits on the exchange. Employees who receive an unaffordable ICHRA, may remain eligible for subsidies.

How Do Excess H&W Dollars Work with ICHRA?

Under a traditional group health plan, a contractor pays a fixed premium and earns fringe credit dollar-for-dollar up to the plan's per-employee cost. If the wage determination requires $5.00 per hour in H&W fringe but the plan costs $6.00, that extra dollar per hour simply disappears, no credit, no return.

ICHRA works differently. Employers set the allowance. If the H&W fringe obligation is $5.00 per hour but an employee's individual premium only runs $3.00, the remaining $2.00 doesn't have to go to waste. Under SCA rules, unused fringe dollars may be applied toward other bona fide benefits, such as life, dental, vision, or retirement contributions, or paid out as cash in lieu of benefits, in accordance with 29 CFR § 4.170.

The result is total fringe optimization. Contractors who size their ICHRA allowances to match their actual H&W obligations, rather than locking into a group plan that may not fit their workforce, can redirect the difference to other qualifying benefits or compensation. Several CVRD clients do this automatically, routing excess fringe to retirement contributions and improving employee benefits without adding a dollar to their cost structure.

How Do Fringe Dollars Fund an ICHRA?

This is where ICHRA gets practical for GovCon finance teams.

Your H&W fringe obligation under the SCA wage determination is a dollar-per-hour amount the contractor must spend on bona fide benefits. Because ICHRA qualifies as a bona fide fringe benefit, those fringe dollars can go directly toward funding the employer's ICHRA contribution. The money you're already obligated to spend on benefits becomes the money that funds employee health coverage.

Here's why the math tends to work in the contractor's favor. Individual market premiums are generally lower than equivalent group plan costs, especially for younger or healthier employees in moderate-cost markets. That means the ICHRA allowance a contractor sets, funded by fringe dollars, often comes in below the average fringe rate specified in the wage determination. The employer meets its full H&W obligation through the ICHRA contribution without overspending relative to the fringe rate.

When the ICHRA contribution does come in below the required fringe rate, the remaining fringe dollars don't disappear. They can be allocated to other bona fide benefits like a 401(k) contribution, or paid out as a cash equivalent in compliance with the SCA. The DOL regulations permit this under 29 CFR § 4.170, provided the contractor meets the total H&W obligation through some combination of bona fide benefits and cash.

The result is a cleaner alignment between what the contract requires and what the contractor actually spends. Instead of paying a group premium that may exceed the fringe rate, the contractor funds an ICHRA at or below the fringe threshold, routes any remaining dollars to additional employee benefits, and keeps total fringe costs predictable. Some CVRD clients use this structure to automatically direct excess fringe dollars into 401(k) contributions, improving total compensation without adding cost.

What Does the ICHRA Adoption Landscape Look Like Right Now?

The market has moved faster than most benefit professionals expected.

Since ICHRA launched in 2020, adoption has grown more than 1,000% from a small baseline at launch, according to HRA Council data. ICHRA adoption increased 34% among large employers and 52% among smaller employers year-over-year in 2025. By current estimates, between 400,000 and 800,000 U.S. workers are enrolled in ICHRA arrangements, a number HealthSherpa projects could triple again by 2027. In a 2026 broker survey, 92.8% of brokers said they believe ICHRA adoption will increase significantly over the next five years.

And once employers make the move, they tend to stay. The HRA Council found that 92% of employers who offered an HRA in one year continued offering it the following year.

For government contractors, adoption is still early, which means the contractors who move now set the standard while competitors are still figuring it out. The generalist ICHRA platforms aren't built for SCA compliance, and the window to differentiate on fringe benefit strategy is open.

What Does the ICHRA Process Actually Look Like?

The implementation process is more straightforward than most contractors expect. Here's a general outline:

1. Model the benefit design. Define which employee classes will be eligible, set allowance amounts by class (aligned to wage determinations where applicable), and establish the plan year.

2. Draft plan documents. ICHRA requires a formal written plan document. This is non-negotiable for SCA bona fide status and ACA compliance. The plan document must describe eligibility, allowances, claims procedures, and notice requirements.

3. Notify employees. Employers must provide written notice to eligible employees at least 90 days before the start of the plan year. The DOL provides model notices for ACA reporting purposes.

4. Enroll employees. Employees need help selecting individual plans, ideally with an advocate who understands the individual market and can match employees to plans that fit their doctors, prescriptions, and budgets.

5. Fund and administer. Employer contributions are funded monthly to the ICHRA administrator. Employee’s enrollment is required to trigger a premium reimbursement. Administrators track spending against allowances and fringe obligations in real time.

6. Comply and report. ICHRA requires ACA 1094/1095 reporting for ALEs. Real-time tracking against wage determination requirements keeps contractors audit-ready without manual spreadsheet reconciliation.

How Does CVRD Handle ICHRA for Government Contractors?

Here's the thing. Most ICHRA platforms aren't built for government contracting. They handle enrollment and reimbursement, but they don't account for the additional compliance requirements that come with running ICHRA under the SCA. Things like per-contract fringe tracking, wage determination alignment, enrollment, administration and tracking of other bona fide benefits (e.g., dental, vision, life, retirement), and DOL audit documentation require purpose-built infrastructure that general ICHRA administrators were never designed to support.

CVRD Health was built specifically for this intersection. The platform models allowances against wage determination requirements, tracks fringe spend per employee in real time, and flags gaps before they become compliance issues. CVRD Health clients have consistently reported lower per-employee benefit costs compared to their prior group plans, reduced administrative burden, and greater predictability in benefit annual spend.

The platform also includes concierge advocacy. Qualified benefits advisors help employees choose individual plans that actually work for their situation. Employees who feel supported in their enrollment decisions are more likely to engage with their benefits and less likely to create noise for HR.

If you're a government contractor looking at your next renewal season and wondering whether there's a better way to structure fringe benefits, the short answer is: there is.

The Bottom Line: What Should You Do Next?

An ICHRA isn't right for every employer in every situation. But for government contractors managing SCA obligations, it deserves a serious evaluation, especially if you're facing group plan renewals with double-digit rate increases, managing a workforce spread across multiple states, or struggling to align benefit costs with contract-specific H&W fringe rates.

Here's what to evaluate before your next renewal:

- What are your current per-employee benefit costs versus the H&W fringe rates in your active wage determinations?

- What would individual market premiums look like for your workforce demographics and geographies?

- Are your current benefits portable for employees, or does everything reset when a contract changes hands?

- Is your current compliance documentation audit-ready if DOL comes knocking?

These aren't hypothetical questions. They're the ones your competitors are starting to ask.

Reach out to CVRD Health to model what an ICHRA structure could look like for your specific contract portfolio. Or explore the related posts below to go deeper on fringe benefit strategy.

Related reading:

- ICHRA vs Group Health Insurance: Why Government Contractors Are Making the Switch

- The Fringe Cringe: Why Government Contractors Are Bleeding Money on Benefits

External sources referenced:

Educate & Engage