How We Let Health Insurance Break(and Why It’s Still Broken)

The Boiling Frog of Health Insurance

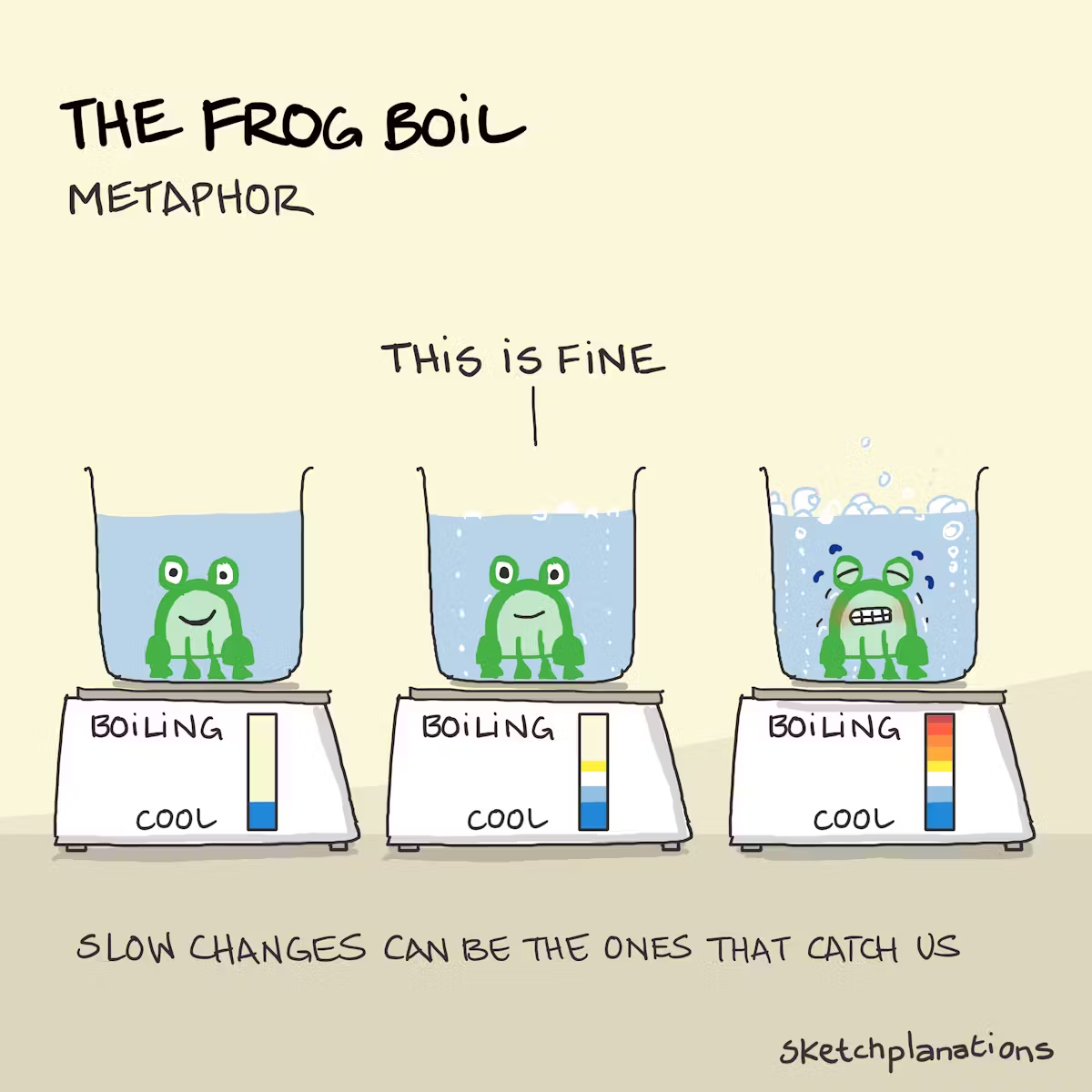

Picture a pot of water heating so gradually that the frog inside doesn’t notice until it’s too late. That’s us with health insurance. Year after year, premiums slowly crept up, coverage subtly got thinner, and we all just sighed and stayed in the pot. Complacency built the current mess we’re in. Employers and employees alike became conditioned to accept annual premium increases as a fact of life, much like rent hikes or our climate changing. In 2024, the average family premium hit about $25,572, up 6% from the prior year, a slow boil few questioned. For context, family premiums in 1996 were about $3,329. We adjusted our budgets, maybe raised deductibles to save a few dollars, but we never jumped out of the pot (or even stopped to ask why the stove was on in the first place).

That complacency led to less pushback and more resignation. An HR manager hears, “Our plan won’t cover my physical therapy,” and shrugs: “Yeah, insurance is tough.” Everyone moves on…but should we? Each time we accept “that’s just how it is,” we reinforce a broken norm. Like the slowly boiling lobster, we’ve adapted to dysfunction instead of demanding change. Over the years, that collective shrug has let insurers make things more complex and expensive with little resistance. Pain points are treated as annoyances instead of alarms. The result: a system so confusing and costly that most Americans think it’s normal to skip care because it’s too expensive, or have no idea what a procedure costs or why a claim was denied. The frog’s fully boiled.

Entitlement vs. Product: Misaligned Mindset, Misaligned Incentives

Another reason we let insurance break is a fundamental mindset issue: we began to view health insurance as an entitlement rather than a product. For many, insurance comes automatically with a job, and different jobs have different options, but we don’t have much say in it because we feel lucky to have insurance at all. We don’t feel we get to actively choose or evaluate our options. When we look at our options as “we’re just lucky to have options at all” we’re less likely to scrutinize what we’re actually getting. We simply assume it covers everything we need it to (and get upset when we realize, typically down the line, that it doesn’t). We also assume high costs are inevitable because healthcare is “supposed” to be expensive. It’s that way for everyone. It’s just the way it is. It’s a strange doublethink: expect more, question less.

Historically, this mindset took root when health insurance became tied to employment during WWII. With wage freezes in effect, companies lured workers by adding health benefits. The government reinforced it with tax breaks. By 1955, over 60% of Americans had employer health insurance (up from just 10% in 1940). Insurance was no longer a personal purchase; it was a standard job perk. Crucially, the employer, not the individual, chose the insurance plan and benefits for workers. We’ve been living with that model ever since. The sense of ownership shifted from patients to institutions. Insurance started feeling like an entitlement of the job (something your company “owes” you) instead of a consumer product you shop for.

Why does this matter? Because when we don’t see ourselves as customers with choice, insurers don’t see us that way either. Their incentives skew toward pleasing the true customer (the employer or the government) rather than the end-user (you, the patient). We end up with insurance designs that serve HR departments’ checkboxes or government regulations more than our actual health needs. And we, the users, mostly go along with whatever plan we’re handed, however mediocre, because it’s what we’re offered. Misaligned perception leads to misaligned incentives: we think insurance should take care of us as if it’s a social safety net, but insurers operate as for-profit product vendors serving someone else. The result is disappointment all around.

How We Lost Price Transparency (HMOs → PPOs → “Networks”)

The largest structural issue within our system is the loss of price transparency. And it didn’t disappear overnight, it eroded as the insurance landscape evolved from simple hospital plans to HMOs, then PPOs, then today’s complex labyrinth of provider networks. If you’re confused, you’re not alone. I challenge you to find one person (who doesn’t work in insurance) who can explain benefits in depth without saying “but that one part, I’m not really sure how that works”. Complexity replaced clarity, largely to protect profits.

Think about it: When was the last time you knew upfront what a medical service actually costs? Probably never. Over the decades, insurance introduced contracted networks and negotiated rates that are nearly impossible for a normal person to decipher. Something that makes things more complex is that there’s different tiers of service costs within systems. In an older era, say the 1960s, you had a basic Blue Cross plan that paid the hospital and you might know the “usual and customary” charge. But then came the HMO (Health Maintenance Organization) in the 1970s-80s with its restricted network and copays, emphasizing preventative care but obscuring actual costs behind set copay amounts. HMOs got a bad rap for gatekeeping and limited choice, so the PPO (Preferred Provider Organization) rose up, offering more provider choice and out-of-network options – at the cost of even more complicated billing. Each provider now had a different price for each insurance contract, and out-of-network charges ballooned. Fast forward: now we have a myriad of “networks” and plan types; every insurer negotiates secret discounts with every hospital and doctor. Patients are literally in the dark. When you get a medical service you will have one of two reactions: a sigh of relief or your heart dropping.

When you shop for insurance today, you’re basically comparing networks and deductibles, not prices of care. It’s almost guaranteed you can’t find out the price of, say, an MRI at various hospitals through your plan. Plans are marketed by features (“$20 copay! Broad network!”) rather than by any notion of value or price. Even after you get care, the bills are indecipherable. You see a $10,000 list price, a mysterious “adjustment” bringing it to $1,000 because of your insurer’s deal, maybe a different amount if you have a different employer plan, and you probably pay a fraction of that as copay. But nowhere can you, the consumer, easily discover the actual price accepted. The hospital and insurer keep those rates under wraps. And it’s always different depending on the plan. On the person. On the day.

Why is this lack of transparency so persistent? Because it’s profitable (and people tend to use more healthcare when they don’t know what it costs). Hospitals and insurers treat price info like trade secrets. They negotiate behind closed doors, and different patients pay wildly different amounts for the same service. In any other market, this would be absurd and unfair – imagine if a cup of coffee had five different prices depending on where you worked and how much coffee you decided, upfront, that you would drink. But in healthcare, that’s standard. It benefits the industry: by keeping us confused, they avoid true price competition. If you can’t easily shop around, providers face less pressure to lower prices, and insurers can claim they’re giving you a “discount” off an inflated sticker price. The complexity protects the profit margins. Unfortunately, it also incentivizes bad behavior, like surprise billing and narrow networks, which further undermine our trust. We end up frustrated by high costs and random coverage gaps, yet we rarely know where to direct that frustration because the root prices are hidden from view.

When Insurance Became Big Business (and People Became Statistics)

Perhaps the biggest structural crack-up came when health insurance shifted from a community service to a big business. In the beginning, it wasn’t like this. Health insurance in America started as a not-for-profit endeavor. In 1929, a hospital administrator in Texas came up with Blue Cross, a nonprofit plan to prepay hospital bills – not to make money, but to keep patients out of bankruptcy and hospitals out of the red. It was simple: one price for all, everyone welcome. The plan provided up to 21 days of coverage for hospitalization annually if patients prepaid 50 cents a month. It was an immediate success, soon enrolling employees across the city. By 1939, Blue Cross had 3 million subscribers and was hugely popular. For a while, insurance really was about spreading risk and helping people afford care.

Two big turning points changed that: medical innovation and World War II. As medical technology advanced (think ventilators, new surgeries in the 1940s), costs went up and insurance had to cover more. Then WWII wage freezes led employers to start offering health benefits to attract workers, with a nice tax break to sweeten the deal. By the 1950s, most working Americans got health insurance through a job, and Blue Cross (nonprofit) dominated. Here’s where business sniffs opportunity: for-profit insurance companies (like Aetna and Cigna) saw a booming market and jumped in. Unlike the nonprofits, they weren’t obligated to cover everyone or keep rates flat – they cherry-picked the young and healthy employees, offered slightly lower premiums, and skimmed off the profitable part of the market. This was great for those companies’ growth, but it undermined the “cover everyone” ethos. Suddenly, insurance wasn’t one big community pool; it was a competition where each company wanted the low-risk customers and would price accordingly.

The nonprofit Blue Cross plans, stuck covering higher-risk folks, started losing out. By the 1990s, they were bleeding money and many decided to convert to for-profit to survive. In 1994 the Blue Cross association changed its rules to allow member plans to become for-profit, and they did – merging and morphing into today’s behemoths like Anthem and Wellpoint. Thus the last big player with a public service mission transformed into just another corporation. When a public-service mission (“affordable care for all”) goes head-to-head with shareholder value, profit tends to win. And it did.

Once insurance became a for-profit game, the industry embraced a new playbook, one that often puts profits over people. Here’s the playbook in a nutshell, as observed by industry experts:

- Tie executive pay to profits: In for-profit insurers, executive compensation skyrocketed into the tens of millions, directly linked to company earnings. How to boost profits when revenue comes from premiums and costs are claims? Simple: raise premiums and cut benefits. We’ve literally seen an insurer propose a 39% premium hike in one year until regulators stepped in. Reducing what they pay out (denying more claims, covering less) also boosts the bottom line. Good for the CEO’s bonus, not so great for your coverage.

- Buy influence with politics: The industry spends over $150 million each year on lobbying our lawmakers. Why? To nudge the rules in their favor or block reforms. When you deal in life-and-death products like health insurance, getting friendly laws (or lax oversight) is a solid investment. Elected officials, who need campaign funds, often listen. This lobbying muscle has helped insurers fend off things like stricter price regulations and maintain their advantageous position.

- Own the system: Why negotiate prices if you can buy out the middlemen and providers? Modern insurers have been on a buying spree, snapping up pharmacy benefit managers, clinics, even doctor groups. In fact, UnitedHealth (the nation’s largest insurer) now employs about 90,000 physicians (roughly 10% of all doctors in the US). That’s huge. Owning providers and pharmacies means the insurer can control (and profit from) more of your healthcare experience. It also locks out competition. If one insurer controls the local doctors and hospitals, good luck to a new insurance startup trying to get a foothold. Fewer competitors often mean higher premiums for consumers.

- Reward shareholders (not patients) with stock buybacks: When these companies have excess cash, do they lower your premium or improve benefits? Nope. They often engage in stock buybacks, spending billions to buy their own stock and thus enrich shareholders and executives. Since 2010, the big insurers have spent around $120 billion on stock buybacks. That’s money not going into lowering healthcare costs or improving customer service, it’s going to Wall Street.

What does this mean for you? It means the chaos and headaches we experience are features, not bugs, of a profit-driven system. Denied claims, ever-narrower networks, and aggressive cost-cutting (like shrinking customer service while swelling legal departments) are often deliberate strategies to protect margins. A former insurance carrier employee described how over time “everyone felt pressure to spend less on members’ claims” and even the internal language shifted, patients became “policyholders,” care providers became “vendors”. In short, the industry mindset changed from “How do we help the sick?” to “How do we maximize our ROI?”. It’s not that insurance execs are cartoon villains twirling their mustaches; it’s that they operate under incentives that prioritize profit within the bounds of law. And currently, much of what frustrates us as patients (high costs, opaque pricing, coverage gaps) is perfectly legal and very lucrative.

The Structural Problem (and Why It Matters)

Understanding how we let health insurance break is key to fixing it. The misaligned incentives we’ve discussed like complacent consumers, the entitlement mindset, hidden pricing, profit-first corporate behavior – it all converges to create a system that often works against the very people it’s supposed to help. So when your coworker says, “Our insurance won’t cover my kid’s specialist visit!”, it’s not just a random failure by your HR or one stingy insurer. It’s a symptom of a structural illness. The system is doing what it was set up (or allowed) to do: contain its costs, maximize its revenue, and confuse you just enough that you throw up your hands instead of demanding better.

The takeaway is a bit liberating: it’s not your fault that navigating insurance is a nightmare. You’re not crazy for feeling like it’s “always been this way.” It has been, in our lifetime at least. But it hasn’t always been that way, and it doesn’t always have to be. The first step to change is seeing the big picture. We got here through a series of choices (and lack of choices) that put profits, complexity, and complacency over transparency, simplicity, and patients. By recognizing that, we can start asking the right questions. Instead of “What’s the cheapest plan that covers X drug?” we ask “Why is this drug so expensive that I need insurance for it at all?” Instead of “Can I get an appointment this week?” we ask “Why do we have so few doctors and so many billing administrators?”. We’re entering a new consumer era of healthcare, one that demands educated, empowered participants. In other words, we start treating health insurance as a product and a system that can be redesigned, not an untouchable entitlement or an act of nature.

Health insurance is broken by design, but designs can change. We let it break by assuming someone else (the government, employers, insurers themselves) was taking care of it. Now that we see the structural cracks, we (patients, employers, voters) can push to realign incentives and rebuild trust. Whether that means demanding price transparency, supporting reforms, or simply being a more informed participant during open enrollment, it starts with understanding that it’s not just you. The chaos was constructed, and it can be deconstructed. In the next part, we’ll dig into one critical facet of that chaos: the dollars and cents. Why does health insurance cost so damn much? And where is all that money going?

Educate & Engage