ICHRA vs Group Health Insurance: Why Government Contractors Are Making the Switch

Your group health plan renewal just landed. Again. The number is higher than last year. Again. And you have about thirty seconds to decide whether to pass the increase to your employees, absorb it yourself, or quietly wonder if there is a better way to do this.

There is.

More and more government contractors are discovering that the Individual Coverage Health Reimbursement Arrangement, or ICHRA (pronounced "ick-rah"), delivers something the traditional group plan cannot: predictable costs, genuine flexibility, and full compliance with the Service Contract Act (SCA) and Davis-Bacon Related Acts (DBRA) prevailing wage requirements. This post breaks down exactly how ICHRA compares to group health insurance, why the numbers are tilting toward ICHRA, and what the switch actually looks like for a government contracting firm.

What Is an ICHRA?

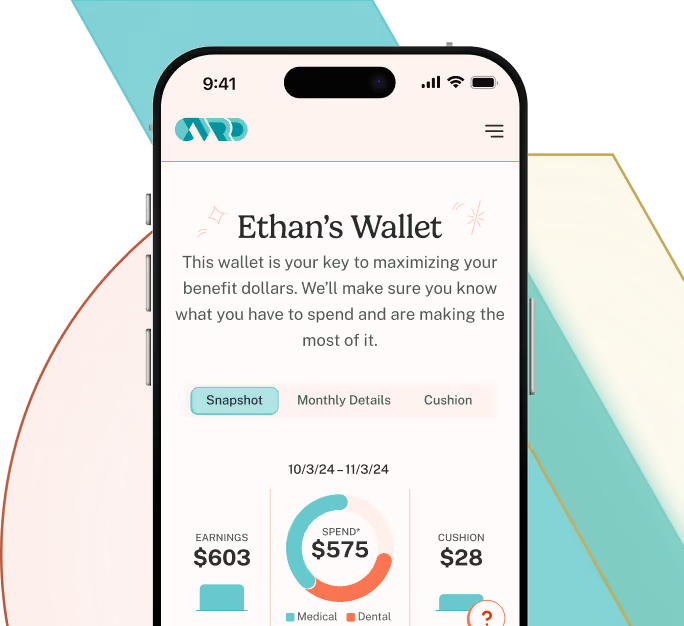

An ICHRA is an employer-funded health benefit where employees receive a fixed, tax-free monthly allowance to purchase their own individual health insurance. Instead of the employer choosing and managing a group plan, employees pick coverage that fits their own doctors, prescriptions, and household situation.

The employer sets the allowance. The employee buys the plan. The employer reimburses. Any unused funds stay with the employer. The IRS requires no minimum or maximum contribution, which gives contractors flexibility to calibrate benefits to different employee classes, such as full-time versus part-time, salaried versus hourly, or employees grouped by geography under SCA wage determinations.

Congress created the ICHRA framework through final rules published by the IRS, the Department of Labor, and Health and Human Services in 2019, with coverage beginning January 1, 2020.

What Is a Traditional Group Health Plan?

A traditional group health insurance plan is an employer-sponsored policy covering a defined group of employees. The employer negotiates with a carrier, selects plan options, and pays a portion of the premiums. Employees contribute through payroll deductions and choose from the options the employer pre-selected.

Group plans require a minimum participation rate, typically 70% of eligible employees. If enrollment falls below that threshold, the carrier can cancel the contract or raise rates. The employer absorbs the risk of premium volatility. When one employee has a catastrophic year, everyone pays for it at renewal.

For government contractors managing large, geographically dispersed workforces under multiple wage determinations, that model creates real problems.

Why Is ICHRA Adoption Growing So Fast?

The numbers are hard to ignore. Since ICHRA became available in 2020, adoption has grown more than 1,000%, according to the HRA Council's 2025 Growth Trends Report. Large employer adoption increased 34% from 2024 to 2025. Small employer adoption rose 52% in the same period. Industry forecasts project 5.8 million covered lives under ICHRA by 2026.

The timing is not a coincidence. Group plan costs are accelerating.

The 2025 KFF Employer Health Benefits Survey found that the average annual family premium reached $26,993 this year, a 6% increase over 2024. That is $1,408 more per employee family than the year before. Mercer's 2025 National Survey of Employer-Sponsored Health Plans found that average employer-sponsored health insurance hit $17,496 per employee in 2025, with a 6.7% increase projected for 2026. That would push the number above $18,500 per employee.

Employer healthcare costs are estimated to be 62% higher in 2026 than in 2017, according to the Business Group on Health.

Government contractors running tight bid margins cannot absorb increases like that year after year.

How Does ICHRA Compare to Group Health Insurance for Government Contractors?

Here is a direct comparison of the dimensions that matter most for SCA and DBRA employers.

Cost Predictability: Who Controls the Budget?

With a group plan, the carrier controls your exposure. You agree to a rate, and your costs shift every year based on claims experience, industry trends, and carrier pricing. Some years it is 5%. Some years it is double digits. You do not find out until renewal.

With ICHRA, you set the allowance. You decide what you contribute, and that number does not change unless you choose to change it. If employee healthcare utilization spikes across your workforce, your costs do not. Your financial exposure is fixed by design.

For government contractors, that predictability translates directly into bid accuracy. When you know exactly what H&W benefit spend will be over the life of a contract, you can price it into your proposal without leaving contingency cushion for premium volatility.

Compliance With SCA and DBRA Fringe Requirements

This is where ICHRA becomes especially powerful for government contractors.

The Service Contract Act, administered under 29 CFR Part 4, requires contractors to provide H&W fringe benefits to covered workers according to rates set in the applicable wage determination. The Davis-Bacon Related Acts impose similar requirements on federally funded construction projects.

ICHRA allowances can count as a bona fide fringe benefit under SCA, satisfying H&W obligations dollar-for-dollar. Employers can structure employee classes under the ICHRA framework to mirror the employee classifications in their wage determinations, full-time versus part-time, salaried versus hourly, workers covered by specific wage determinations versus those who are not.

That alignment between ICHRA class rules and SCA employee classifications is something a traditional group plan cannot replicate cleanly. Group plans require a single policy covering a defined group. ICHRA lets you design benefits around the workforce you actually have.

Participation Requirements: A Hidden Landmine in Group Plans

Group plans require a minimum participation rate, often 70% of eligible employees. That threshold can be difficult for government contractors with variable workforces, high turnover rates, or large numbers of part-time and seasonal workers.

If participation drops below the threshold, the carrier can restructure your contract or walk away entirely. That is not a hypothetical risk. It is a recurring problem for contractors whose workforce composition shifts across contract cycles.

ICHRA has no participation requirement. Any number of employees can participate, and those who decline simply do not receive the allowance. There is no minimum to hit, no participation math to manage.

Employee Choice and Multistate Workforces

Government contractors rarely operate in a single city. You have employees spread across multiple states, military installations, and contract sites, each with different local insurance markets, provider networks, and premium pricing.

A traditional group plan purchased for a workforce in Virginia may not offer meaningful options for employees in Arizona, Texas, or Hawaii. The network is designed around one region. Employees in other states end up with limited choices or out-of-network costs.

ICHRA resolves this structurally. Each employee purchases a plan from their local market. A worker in Boston buys from the Massachusetts exchange. A worker in San Antonio buys from Texas. Both receive the same tax-free allowance. Both get local coverage that actually works.

Administrative Burden: Simpler Than You Think

Group plan administration involves carrier negotiations, open enrollment logistics, mid-year qualifying life events, COBRA administration, and a renewal process that typically consumes significant HR bandwidth.

ICHRA shifts those administrative tasks away from the employer. Employees purchase and manage their own coverage. The employer's obligation is to set the allowance, verify individual coverage enrollment, and process reimbursements or direct payments.

That does not mean ICHRA is zero-effort. Applicable Large Employers (ALEs), those with 50 or more full-time equivalent employees, must still satisfy ACA reporting requirements using Forms 1094-C and 1095-C. Affordability testing is required using age-rated local premiums. And employees need support navigating the individual market, especially if they are new to shopping for their own coverage.

For 2026, the ICHRA affordability threshold is 9.96% of household income, meaning the employer's allowance must be sufficient to make the lowest-cost silver plan on the ACA exchange affordable to each employee. That calculation is individual, not group-level, which requires attention.

Here is the practical reality: most contractors using ICHRA work with a platform or administrator that handles the affordability math, reimbursement processing, and employee enrollment support. The administrative burden shifts, but it does not disappear. The right partner makes the difference.

What Does the Switch Actually Look Like?

Here is what most contractors get wrong about switching from a group plan to ICHRA. They assume it is a single decision that happens at open enrollment. It is not. It is a phased process that works best when started four to six months before the desired effective date.

The core steps are:

- Model the current H&W spend and map it against what an ICHRA allowance would need to look like to be affordable for each employee class.

- Define employee classes using the ICHRA framework, aligning them with your SCA wage determinations and workforce structure.

- Choose an ICHRA administrator to handle reimbursement processing, affordability verification, and compliance.

- Provide employees with a 90-day advance notice, as required by IRS guidance, explaining the new benefit structure and how to purchase individual coverage.

- Support employees through enrollment with advocacy and plan selection assistance, especially first-time individual market buyers.

The employee advocacy piece deserves emphasis. A worker who has been on a group plan for ten years may never have selected their own health insurance. The transition can feel overwhelming without guidance. Contractors who invest in that support see better enrollment outcomes and higher employee satisfaction with the new model.

What About Employees? Do They Actually Prefer ICHRA?

The data suggests they do, when it is implemented well.

A 2025 survey of 2,000 Americans commissioned by Oscar Health found that 44% of workers preferred an ICHRA-style model over traditional employer health insurance, making it the most preferred option among respondents. Among those with current employer coverage, 60% said the coverage did not meet their specific needs very well.

Employees want plans that match their doctors, their family situations, and their budgets. A one-size-fits-all group plan cannot deliver that. ICHRA can.

The portability factor also matters in government contracting, where workforce transitions between contracts are common. Under a group plan, employees lose coverage when they transition off a contract. Under ICHRA, the individual plan belongs to the employee. They carry it with them. That continuity reduces disruption for employees and reduces COBRA obligations for the contractor.

How Does CVRD Approach This?

CVRD was built specifically for this intersection, where ICHRA administration meets government contract compliance. The platform models allowances against your actual SCA wage determinations, structures employee classes to match your contract workforce, and tracks H&W spend in real time so you have the DOL transparency you need.

For contractors running ICHRA through CVRD, the average savings run more than $3,000 per employee per year, with a 31% reduction in administrative costs and more than 27% less volatility in year-over-year benefit spend.

Most importantly, CVRD handles the advocacy layer. When employees log in to choose a plan, they are not on their own. Concierge advocates walk them through the options, help them match plans to their needs, and stay available year-round for questions and changes.

That is the combination most generalist ICHRA platforms cannot offer, defined-contribution flexibility built on top of deep SCA and DBRA compliance expertise.

Is ICHRA Right for Every Government Contractor?

Not automatically. The model works best for contractors who:

- Have geographically dispersed workforces across multiple states or installations

- Struggle with renewal volatility or high turnover affecting participation rates

- Want to align H&W fringe contributions more precisely with SCA wage determinations

- Have a workforce mix of full-time, part-time, and seasonal workers that does not fit neatly into a single group plan

For contractors with a small, stable workforce concentrated in one metro area, a well-structured group plan may still make sense. The honest answer is that it depends on your workforce profile and your bid environment.

What is clear is that the default assumption, that group coverage is the only viable path to SCA compliance, is no longer accurate. ICHRA is a fully compliant, increasingly mainstream alternative. The contractors figuring that out now will have a structural advantage in their benefit cost modeling going forward.

The Bottom Line

ICHRA adoption grew more than 1,000% in five years. Large employers increased adoption 34% in 2025 alone. The reason is not novelty. It is cost control, flexibility, and compliance fit that traditional group plans cannot match, especially for the complex, variable workforces that government contracting requires.

The defined-contribution model has already transformed retirement benefits. The 401(k) replaced the pension. The same shift is happening in health benefits, and government contractors are well positioned to lead it.

If you want to understand whether ICHRA makes sense for your specific contract profile and workforce, reach out. A conversation about your current H&W spend and bid structure is the right place to start.

Related reading: The Fringe Cringe: Why Government Contractors Are Bleeding Money on Benefits

References

- HRA Council, Growth Trends for ICHRA and QSEHRA, Volume 4 (2025)

- KFF, 2025 Employer Health Benefits Survey

- Mercer, 2025 National Survey of Employer-Sponsored Health Plans

- Business Group on Health, 2026 Employer Health Care Strategy Survey

- U.S. Department of Labor, EBSA, HRA Final Rules

- 29 CFR Part 4, Service Contract Act Regulations

- IRS Forms 1094-C and 1095-C, ACA Reporting

- Healthcare Dive, ICHRA Growth Among Insurers (April 2026)

- Oscar Health / Talker Research, Employee Health Insurance Survey (2025)

Educate & Engage