The Fringe Cringe: Why Government Contractors Are Bleeding Money on Benefits

Here's a question most government contractors never think to ask: when was the last time you checked whether your fringe benefit spend actually matches your fringe obligation?

If the answer is "never," or "we just renew the group plan every October and hope for the best," you're probably leaving real money on the table. Possibly thousands of dollars per employee, per year.

There's a name for this. We call it the Fringe Cringe: the slow, grinding realization that the system you've been using to manage Health & Welfare (H&W) benefits was never actually designed for the way government contracting works. It costs you on renewals. It costs you on bids. And it costs your employees, who deserve better options than whatever the group carrier decided to offer this year.

The good news is the math can work in your favor, if you understand what's actually going wrong.

What Are Fringe Benefits Under the Service Contract Act?

The Service Contract Act (SCA), formally the McNamara-O'Hara Service Contract Act, requires federal contractors performing services on government contracts above $2,500 to pay their covered employees at least the locally prevailing wage rate, plus a separate Health & Welfare (H&W) fringe benefit.

An H&W fringe benefit is a mandatory hourly contribution toward employee benefits. It is entirely separate from the employee's base wage.

As of July 7, 2025, the standard SCA H&W fringe rate is $5.55 per hour (up from $5.36 per hour). For contracts also subject to Executive Order 13706 paid sick leave requirements, the rate is $5.09 per hour. That fringe obligation applies to all hours paid, including vacation and holiday time, up to 40 hours per week and 2,080 hours per year, per employee.

Do the math: $5.55 × 2,080 hours = $11,544 per employee, per year in required H&W fringe benefit spend.

That number matters. And most contractors aren't getting full value from it.

Why Is the Standard Group Plan Model Broken for GovCon?

Does a one-size-fits-all group plan actually fit your workforce?

Here's the structural problem: the SCA's H&W fringe obligation is calculated on a per-employee, per-hour basis. It cannot be averaged across your workforce. Under 29 CFR § 4.175, you must satisfy the obligation at the individual employee level.

But most group health insurance plans don't work that way. Group plans price risk across the entire enrolled population, charge fixed premiums per tier (single, employee + spouse, family), and renew on a calendar that has nothing to do with your contract cycle.

So what happens? You end up with a mismatch:

- Employees who elect family coverage cost far more than the fringe rate covers.

- Employees who elect single coverage may cost far less, with the difference going nowhere useful.

- Employees who waive coverage altogether receive nothing (or cash-in-lieu that triggers payroll taxes).

- Employees in different states, different health situations, and different life stages all get crammed into the same plan options.

The group plan was designed for a stable commercial employer with a consistent workforce profile. Government contractors operate with variable workforces, multi-state contracts, and SCA wage determinations that change at option year renewals. The fit was never great. It's getting worse every year.

How Much Is the Mismatch Actually Costing You?

What does a bad fringe structure cost per employee?

The numbers are significant. According to the 2025 KFF Employer Health Benefits Survey, the average annual premium for family health coverage hit $26,993, a 6% increase from 2024, and 53% higher than it was a decade ago. Average single coverage premiums reached $9,325.

Those are averages. Your group plan, covering a GovCon workforce with age and geographic variation, probably looks different. But here's the pattern we see consistently:

The cash-in-lieu trap. Many contractors, trying to simplify compliance, pay the fringe requirement as cash in lieu of benefits, essentially adding $5.55/hour directly to paychecks. It sounds clean. It isn't. Cash wages are subject to FICA, FUTA, SUTA, and workers' compensation. Paying $11,544 per year in cash fringe instead of routing it through a bona fide benefit plan can add 7-10% in employer payroll taxes on top of that amount. That's $800 to $1,150 per employee, per year, straight out of your margin. At scale, across a 200-person contract workforce, that's $160,000-$230,000 in unnecessary tax exposure annually.

The overpay problem. When your group plan costs more than your fringe obligation for certain employee classes, you're subsidizing the gap out of overhead. When it costs less, you may be pocketing the difference, but often not tracking it, and sometimes inadvertently shortchanging employees in ways that create audit exposure.

The renewal ratchet. Group plan premiums increase every year. Your SCA fringe rate (set by the DOL) increases, but not at the same rate or on the same schedule. Every October renewal, the gap between what the carrier charges and what the wage determination covers either widens or tightens, and most contractors find out which when the renewal invoice arrives. That's not a benefits strategy. That's a surprise.

What Counts as a Bona Fide Fringe Benefit Under the SCA?

What qualifies as a bona fide fringe benefit?

A bona fide fringe benefit, under 29 CFR § 4.171, is an employer contribution to a genuine benefit plan that provides real value to employees. This includes health insurance, life insurance, disability insurance, pension, vacation, sick leave, and similar benefits.

What does not qualify as a bona fide fringe benefit:

- Cash wages (these increase your payroll tax burden and don't protect the tax-preferred status of the contribution)

- Workers' compensation premiums (required by law, you can't take SCA credit for legal mandates)

- Administrative costs for payroll processing, record keeping, or W-2 preparation (per 29 CFR § 4.172, administrative costs are your business expense, not creditable toward fringe)

- Relocation expenses, travel reimbursements, or convenience-of-the-contractor facilities

The SCA's fringe rules are designed to ensure employees receive actual benefits, not accounting maneuvers. DOL auditors know the difference, and contractors who blur the line face back-pay liability, civil penalties, and in serious cases, debarment from future federal contracting work.

Why Government Contractors Keep Getting This Wrong

What causes the fringe benefit gap?

Most contractors don't set out to mismanage their fringe spend. They get it wrong because the problem is structural, not behavioral:

1. Contract complexity. A mid-sized GovCon might hold five to fifteen active contracts, each with a different wage determination, a different H&W rate, and a different option-year renewal schedule. Tracking fringe obligations across all of them, against actual benefit spend, per employee, per contract, per pay period — is genuinely hard without the right systems.

2. The group plan default. The path of least resistance has always been to pick a group carrier, cover the workforce, and hope the costs roughly match the fringe obligation. For a long time, that worked well enough. It doesn't anymore. Premiums have risen 53% in a decade. The SCA rate is a floor, not a ceiling — if your plan costs more, the difference comes out of your pocket.

3. Workforce variability. SCA-covered workers are often part-time, seasonal, or rotate across contracts. Group plans don't accommodate this well. ICHRA — the Individual Coverage Health Reimbursement Arrangement — does, because it allows employers to set defined contribution amounts per eligible class of employee, and employees choose their own coverage from the individual market.

4. No real-time visibility. Spreadsheets break down when you're tracking fringe dollars across multiple contracts, wage determinations, and benefit elections. Without real-time data on what you're spending versus what you're obligated to spend, overpayments and underpayments accumulate invisibly until someone runs a year-end reconciliation — or a DOL audit runs it for you.

What Does "Fringe Optimization" Actually Mean?

How do you fix a broken fringe benefit structure?

Fringe optimization means aligning your H&W contribution strategy with your actual SCA obligations — so every dollar you're required to spend on fringe actually reaches your employees in the most tax-efficient, administratively defensible way possible.

In practice, this typically means:

Moving from cash-in-lieu to bona fide plans. For employees currently receiving fringe as cash wages, transitioning to a bona fide benefit plan eliminates the associated payroll taxes and gives employees access to real coverage. The same dollars go further.

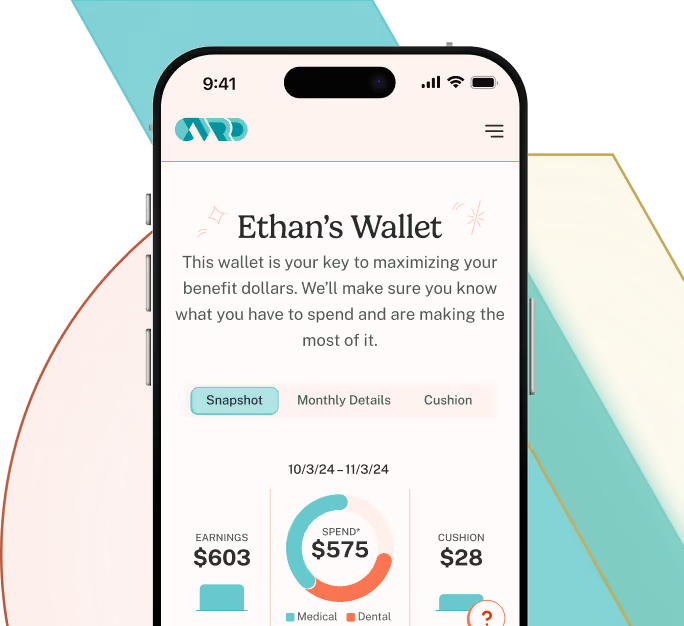

Using ICHRA to match contributions to obligations. An ICHRA — an Individual Coverage Health Reimbursement Arrangement — lets employers set a defined allowance per employee class, and employees use that allowance to buy individual market coverage of their choosing. For GovCon employers managing multi-class workforces across multiple contracts, ICHRA provides flexibility that group plans can't match. The employer contribution is fixed; the employee choice is not.

Tracking fringe spend in real time. Per-employee, per-contract fringe tracking eliminates the year-end surprises. It also creates an audit-ready record of compliance — exactly what DOL wants to see in an SCA fringe audit.

Routing excess fringe to 401(k) contributions. When H&W benefit costs come in below the fringe obligation for certain employees, those excess dollars don't have to disappear. A well-structured fringe program can route them to 401(k) contributions or other qualifying benefits — giving employees more and keeping the contractor compliant.

How CVRD Approaches Fringe Optimization

CVRD built its platform specifically for this problem. The company's fringe benefit optimization platform converts unpredictable H&W spend into a defined cost model — eliminating the group plan's fixed-cost risk while maintaining full SCA compliance.

The typical result: contractors working with CVRD see an average of $3,000+ in premium savings per employee per year, along with a 31% reduction in administrative costs and 27%+ reduced cost volatility compared to traditional group coverage. The platform also provides real-time DOL transparency, so every dollar of fringe spend is tracked, reportable, and audit-ready.

If you've been running the group plan renewal cycle on autopilot, it's worth a conversation to see what the numbers actually look like for your contracts.

The Bottom Line

The fringe cringe is real, and it's expensive. A $5.55/hour H&W obligation, applied across a workforce of any meaningful size, represents a substantial amount of money. Contractors who treat it as a compliance checkbox — renewing the group plan, paying cash-in-lieu, and hoping the DOL doesn't look too closely — are leaving real dollars behind and taking on unnecessary risk.

The fix isn't complicated in principle. It requires knowing exactly what you're obligated to spend, per employee, per contract. It requires delivering those dollars through bona fide benefit plans that give employees real value. And it requires visibility into the numbers in real time, not once a year at renewal.

Here's the thing: government contracting is competitive. Margins are tight. Every dollar of fringe you waste on unnecessary taxes, carrier overhead, or cash-in-lieu inefficiencies is a dollar that doesn't go to your people — and doesn't come back to your bottom line.

There's a better way to run this.

Ready to see what your fringe spend actually looks like? Get in touch.

External references:

DOL Fact Sheet #67B: Meeting SCA Fringe Benefit Requirements

2025 KFF Employer Health Benefits Survey

DOL Wage and Hour Division: 2025 SCA H&W Rate Update (AAM 250)

Educate & Engage