ICHRA Employee Classes Explained: How GovCon Employers Can Customize Benefits

Most government contractors have a workforce that looks nothing like a neat organizational chart. You have SCA-covered hourly workers in the field, salaried project managers in the office, and a handful of employees scattered across three time zones. Most contractors pay $5.09 per hour, but one group has a prevailing wage fringe obligation of $5.55 per hour. Another group has no fringe mandate at all. And you've been trying to run them all through the same group health plan.

Here's what most people don't realize: ICHRA (Individual Coverage Health Reimbursement Arrangement) was designed with exactly this kind of workforce in mind. The class system built into the ICHRA rules is one of the most practical tools in GovCon benefits, and almost nobody uses it to its full potential.

This post explains what employee classes are, how they work, and how government contractors can use them to stop overpaying on benefits while staying fully compliant.

What Is an ICHRA, and Why Do Classes Matter?

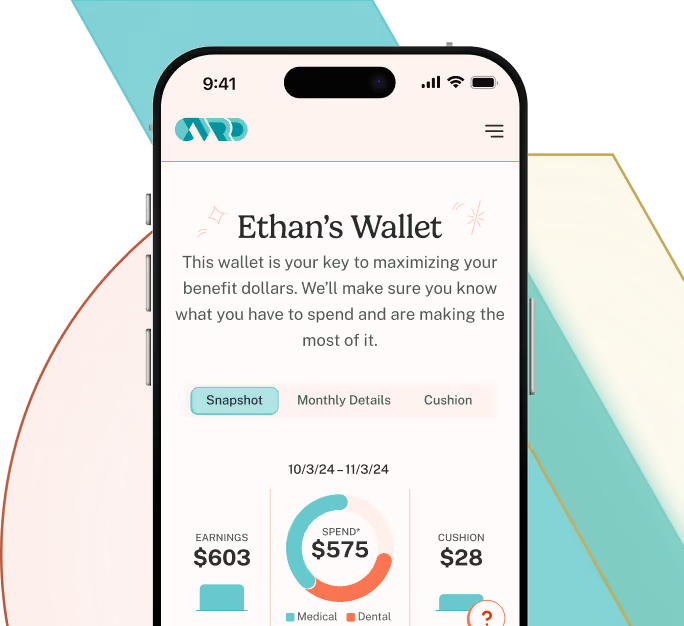

An ICHRA is an employer-funded benefit that allows companies to reimburse employees for individual health insurance premiums and eligible medical expenses on a tax-free basis. Instead of buying a single group plan and forcing everyone into it, the employer sets a monthly allowance and employees shop for the plan that fits their situation.

The ICHRA Final Rules, published in June 2019 and effective for plan years beginning January 1, 2020, gave employers the ability to divide their workforce into up to 11 distinct employee classes. Each class can receive a different reimbursement amount. Each class can be offered ICHRA, a traditional group plan, or nothing at all.

That classification system is the key to making ICHRA work for a government contractor. Without it, you're still offering a one-size-fits-all benefit to a workforce that is anything but one-size.

What Are the 11 ICHRA Employee Classes?

The classes are defined at 26 CFR § 54.9802-4(d)(2) and are based on objective, job-related criteria. Here is the complete list:

Classes cannot be based on job title, health status, or any discriminatory factor. They must reflect legitimate, objective job-related distinctions.

Why This Matters Specifically for Government Contractors

Government contractors often operate workforces with genuinely different benefit situations sitting under the same roof. ICHRA classes let you treat those differences honestly instead of papering over them with a single group plan.

Here are three scenarios where classes solve a real problem.

How Do You Handle SCA Hourly Workers Differently from Salaried Staff?

This is the most common challenge CVRD sees with GovCon clients.

Your Service Contract Act (SCA)-covered hourly employees have a mandated fringe benefit obligation. As of July 7, 2025, that H&W rate is $5.55 per hour under DOL All-Agency Memorandum 250, or $222 per week. Your salaried employees have no such mandate.

With ICHRA classes, you can create two separate benefit designs:

- For SCA hourly workers: Set the monthly ICHRA allowance to meet or closely match the fringe obligation. This satisfies the DOL's bona fide fringe benefit requirement and, critically, puts those dollars to work as tax-free benefit dollars rather than straight cash wages.

- For salaried employees: Set a different allowance level based on your budget and the local cost of individual coverage. No fringe mandate to meet. No group plan to overpay for.

Both groups get a real benefit. You stop cross-subsidizing one group with the other. And because each class has a defined dollar amount, your benefit cost is predictable at renewal, no surprises.

What If You Have Employees in Multiple States?

Geographic classes are one of the most powerful and underused features of ICHRA.

Group health insurance is priced by rating area. If you have a group plan anchored in, say, Virginia, your employees in Texas or Florida are likely covered by a plan with a network that barely works for them, at a premium that doesn't reflect their local market.

ICHRA geographic classes let you create separate benefit designs for employees in different rating areas. You can offer $600 per month to employees in a high-cost market like the San Francisco Bay Area and $400 per month to employees in a lower-cost region, all within the same ICHRA. Each group shops in their own local market and picks a plan with in-network providers near where they actually live.

Important note: geographic classes based on rating areas smaller than a state do carry minimum class size requirements (more on that below). State-level geographic classes are exempt from those minimums.

Can You Offer Both a Group Plan and ICHRA at the Same Company?

Yes, with one important constraint: you cannot offer both a traditional group plan and an ICHRA to the same class of employees. You can offer group coverage to one class and ICHRA to another, as long as those classes are clearly defined and the distinction reflects a legitimate business reason.

A common setup for government contractors: offer ICHRA to SCA-covered hourly employees (where it matches the fringe obligation cleanly) and keep a group plan for salaried corporate staff who prefer that arrangement. That structure is fully permitted under the ICHRA rules. What it is not permitted to do is cherry-pick, keeping the healthiest employees on the group plan while routing higher-risk employees to individual coverage. That is exactly what the minimum class size rules are designed to prevent.

What Are the Minimum Class Size Requirements?

Minimum class size rules apply when you are offering both a traditional group plan and ICHRA to different employee classes. If you are offering ICHRA only, no minimums apply.

The minimums, per 26 CFR § 54.9802-4(d)(3), are:

These minimums apply to the following classes: salaried, non-salaried (hourly), full-time, part-time, and employees in the same geographic rating area (when the rating area is smaller than a state). Seasonal workers, CBA employees, employees in waiting periods, foreign employees, and temp workers from staffing firms are exempt from minimum size rules.

How Can You Vary Allowance Amounts Within a Class?

Within each class, all employees must receive the ICHRA on the same terms. That is the nondiscrimination rule. But "same terms" does not mean "same dollar amount." You are permitted to vary the monthly allowance within a class based on two factors:

Age. Older employees typically pay higher premiums for individual coverage. The ICHRA rules allow you to set higher allowances for older employees within a class, subject to a 3:1 ratio limit. You cannot offer a 60-year-old more than three times the allowance you offer a 21-year-old in the same class.

Family status. You can offer different allowance amounts based on whether an employee is self-only, covering a spouse, covering dependents, or covering a full family. That flexibility matters in GovCon, where many SCA workers are supporting families and the cost of adding dependents to individual coverage can vary significantly by market.

For 2026, the IRS has set the following maximum ICHRA reimbursement limits: $6,450 per year ($537.50 per month) for self-only coverage and $13,100 per year ($1,091.67 per month) for family coverage. These caps represent the maximum a contractor can reimburse tax-free. There is no requirement to hit the maximum.

What Compliance Boxes Does This Check for Government Contractors?

ICHRA classes align well with the compliance obligations government contractors already manage.

SCA fringe compliance. Under the McNamara-O'Hara Service Contract Act, contractors must pay the H&W fringe rate in either cash or bona fide benefits. ICHRA qualifies as a bona fide fringe benefit plan. By setting the ICHRA allowance for SCA hourly workers to match the prevailing H&W rate, contractors can satisfy the fringe obligation while giving employees something genuinely useful. The employee gets a tax-free health benefit. The contractor avoids paying the fringe rate as additional taxable wages.

ACA employer mandate. For applicable large employers (those with 50 or more full-time equivalent employees), ICHRA must meet the ACA affordability standard to satisfy the employer mandate and avoid penalties. In 2026, that means the employee's required contribution toward the lowest-cost silver plan in their area, after applying the ICHRA allowance, cannot exceed 9.96% of their household income. The class structure helps here. Because geographic classes allow you to calibrate allowances to local market costs, you can hit the affordability threshold in each market without over-funding every class to the level of your most expensive location.

DOL audit readiness. The same real-time tracking and documentation that helps contractors stay current on fringe obligations also supports ICHRA class administration. Every allowance, every employee class assignment, and every reimbursement should be documented and traceable. Spreadsheet-based approaches break down fast when you have multiple classes across multiple contracts.

Building a Class Structure That Actually Fits Your Workforce

There is no single right answer on how many classes to create or how to define them. The right structure depends on your workforce composition, your contract mix, and your budget.

That said, a few practical principles hold across most GovCon situations:

Start with the SCA hourly versus salaried split. That is the most common distinction that creates a genuine benefit design difference. SCA workers have a fringe floor. Salaried employees do not. Build separate classes from the start.

Add geographic classes if you operate in multiple markets. If you have employees in high-cost markets like New York, California, or Washington, D.C., alongside lower-cost markets in the Southeast or Midwest, geographic classes let you match allowances to actual premium costs instead of funding everyone at the highest-cost level.

Use combination classes for precision. If you have part-time SCA workers in a specific region, you can create a "part-time employees in [state]" class that gives you granular control over that benefit. The IRS permits any combination of the 11 base classes.

Review annually. Under 26 CFR § 54.9802-4(d)(2), class definitions must be set before the plan year begins and cannot be changed mid-year. Build your structure during the design phase, not after enrollment.

How CVRD Helps Contractors Design and Manage ICHRA Classes

Designing a class structure on paper is one thing. Running it in real time across a workforce with SCA obligations, multiple contract vehicles, and a rotating roster of employees is another.

CVRD builds custom allowance models for government contractors that account for the fringe obligation on each contract, the local premium environment for each employee class, and ACA affordability requirements. Contractors working with CVRD have seen an average of $3,000 in premium savings per employee per year, along with a 31% reduction in administrative costs and more than 27% reduced volatility at renewal time.

The platform tracks fringe spend in real time, which means compliance documentation is always current, not assembled from memory six months after the fact.

If you want to see what a class structure designed for your specific workforce would look like, reach out. There is no obligation. We just think you should see the numbers before your next renewal.

Quick Reference: ICHRA Employee Classes for Government Contractors

- There are 11 IRS-defined classes, codified at 26 CFR § 54.9802-4

- Classes must be based on objective, job-related criteria

- Different classes can receive different monthly allowance amounts

- Within a class, allowances can vary only by age (3:1 ratio) and family status

- Minimum class size rules apply only when offering both ICHRA and a traditional group plan

- Geographic classes are particularly useful for contractors with multistate workforces

- ICHRA satisfies the SCA bona fide fringe benefit requirement

- Class definitions must be set before the plan year and cannot change mid-year

- ICHRA adoption has grown 2.8x in the past year as employers discover the flexibility

Related reading:

- ICHRA for Government Contractors: The Plain-English Guide

- ICHRA vs Group Health Insurance: Why Government Contractors Are Making the Switch.

Sources:

- 26 CFR § 54.9802-4, ICHRA Final Rules

- Federal Register: Health Reimbursement Arrangements Final Rule (June 2019)

- DOL All-Agency Memorandum 250: 2025 SCA H&W Rate Update (July 2025)

- DOL SCA Wage Determinations Overview

- IRS Affordable Care Act Employer Mandate Information

- Take Command Health: 2026 ICHRA Employee Classes

- PilieroMazza: 2025 SCA Health and Welfare Rate Increase

Educate & Engage